Stock slide continues as markets await inflation data

Headlines

* US GDP annualised disappoints at 1.3% versus 1.6% expected

* Dollar and yields lower as safe haven CHF and JPY rally

* Stocks fall as Salesforce plunges and investors brace for inflation

* OPEC+ working on complex production cut deal for 2024-2025

FX: USD gave back most of Wednesday’s gains. The second estimate of US GDP printed at 1.3% versus expectations of 1.6% and 3.4% in the last quarter of 2023. Friday’s inflation data is firmly in focus. The 10-year US Treasury yield turned down after moving above 4.60%.

EUR tapped the strong zone of support just below 1.08 that we mentioned yesterday, before rebounding strongly. EZ unemployment dipped to 6.4% from 6.5% so bolstering the ECB hawks worried about wage growth and second-round effects. The zone’s CPI is published today.

GBP found support around 1.27. Again, there was little GBP news, with dollar selling helping the major. The first round of polls since PM Sunak called an election showed no major change. It’s still Labour’s election to lose. Last week’s high is at 1.2800.

USD/JPY turned lower after threatening to break higher on Wednesday. Prices have dipped below the major Fib level (61.8%) at 157.01 of the recent high/low during the recent period of FX intervention. Safe haven currencies outperformed, with the CHF supported by SNB’s Jordan remarks saying that a weaker currency is now the most likely source of higher Swiss inflation.

AUD picked up, bouncing off support levels around 0.66 and ignoring a sharp slide in iron ore. USD/CNH turned lower after heading into resistance above 7.27. USD/CAD moved lower with prices back to the 50-day SMA at 1.3658. Markets have half an eye on the Bank of Canada meeting next Wednesday. There are around 16bps of a rate cut priced in, or a 64% chance.

US Stocks: Indices closed lower with tech dragged lower by Salesforce dismal update. The S&P 500 finished lower by 0.60% at 5,235. The Nasdaq 100 settled 1.06% down at 18,539. The Dow closed in the red by 0.86% at 38,111. Salesforce plunged nearly 20% after it reported its first revenue miss since 2006. The customer relationship management software provider also offered a downbeat outlook for the ongoing three-month period. Tech was by far the biggest losing sector, off 2.45%, while utilities and real estate posted gains of over 1.4%.

Asian Stocks: APAC futures are lower. Asian stocks were down after the poor handover from Wall Street. The ASX 200 was under pressure from underperforming miners after recent declines in commodities. The Nikkei 225 dipped briefly below the 38,000 level but settled off its worst levels. China stocks were subdued with weakness in Hong Kong property stocks. The mainland was helped again by a big liquidity injection by the PBoC.

Gold found support at the 50-day SMA at $2324. The pullback in yields helped bullion. Real yields had risen to levels last seen in 2007.

Day Ahead – Inflation Day

US PCE data is the big risk event of the day, though eurozone and Tokyo consumer price data will be important. Theheadline US PCE prices are seen rising at an unchanged rate of 0.3% m/m in April. The annual rate is expected to be steady at 2.7%. The key core measure is seen rising 0.2% m/m, a tenth lower than the prior. The annual core PCE is also seen unchanged at 2.8% y/y.

Headline CPI data was cooler than expected in April, while the core CPI metric saw the smallest increase since December. Meanwhile, the PPI data for the month surprised to the upside. But economists noted that the internals and components that feed into the PCE data were more constructive. Rate cut bets have been reined in recently with the chances of a September move now near 50:50.

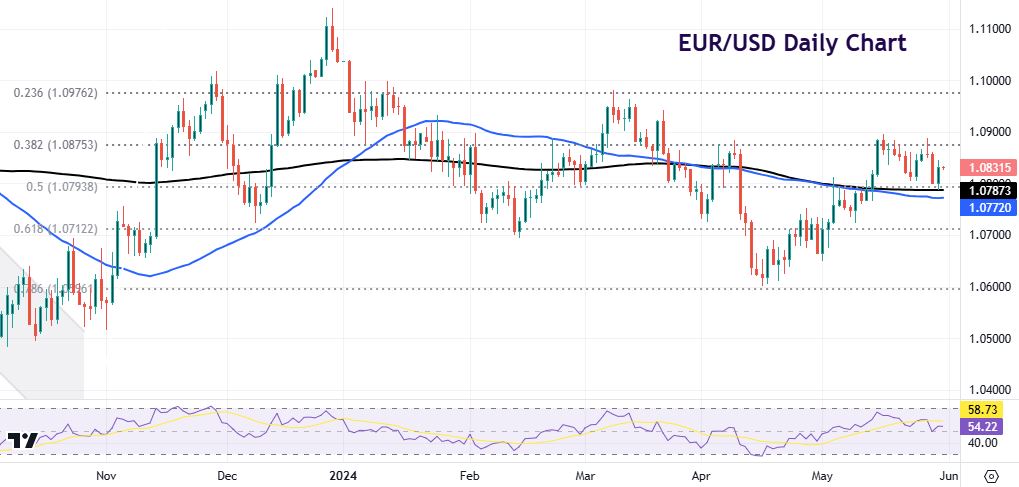

Chart of the Day – EUR/USD eagerly awaits price data

Consensus forecast eurozone headline CPI to have risen one-tenth to 2.5% y/y due to higher energy prices. The core metric is set to hold steady at 2.7% y/y. The prior release saw the headline unable to make much progress, remaining at 2.4% amid an increase in food inflation and only a modest decline in energy inflation. The core print fell two-tenths from 2.9% due to moderating services inflation.

The ECB is nailed on to cut rates in June according to market pricing, with policymakers also endorsing this move in recent weeks. However, traders may opt to continue scaling back expectations of what happens after, especially on a relatively hot report. A strong support zone, which includes the midway point of the Q4 rally and the 200-day SMA, sits just below 1.08. Resistance is around the next Fib level at 1.0875.